Fundamentals out the Window? Hedge Funds (Selectively) Still Work

The old argument for hedge funds used to be fairly simple and centred around “would you rather be constrained (e.g. long-only) or unconstrained (have the option to be both long and short)”? The further explanation was that the expertise of managers to carefully analyse securities would enable them to construct a portfolio of quality long positions in companies with positive outlooks and reasonable prices, then offset that with a short book consisting of securities with negative outlooks, mispriced on the high side. Today’s environment is proving to be a challenge for those that hold on to the notion that price should be reflective of underlying fundamentals. Perhaps it is merely a respite, but it seems that momentum, fuelled by a massive government cash influx, a willingness to take a long term view, and the decision to ignore analysis building blocks like DCF models, is ruling the new normal. The absence of fundamentals warrants a closer examination, particularly as relates to investment in traditional and alternatives strategies.

The term “fundamentals” itself deserves a bit of attention. The fundamentals that are important here are economic fundamentals primarily affecting the macroeconomic environment, more sector and strategy fundamentals that might impact portions of investment portfolios or steer an allocation, and finally the more often thought of corporate or security specific fundamentals affecting specific public/private capital structures both absolutely and relatively. It is an unusual period in which none of these three types of fundamentals seem to matter to all types of asset prices. While equity investors have become inured to growth stock valuations that seem to defy logic (or at least a timeline to profits), this type of forward view now seems to pervade many corners of the investment universe. In fact, the search for yield coupled with ample capital willing to finance all but the dodgiest of corporates/projects, has now made fixed income difficult to analyse for both long and short opportunities. Given that fundamentals are at best less important, the question that needs to be dealt with is which style of investment will continue to function most effectively in the current environment?

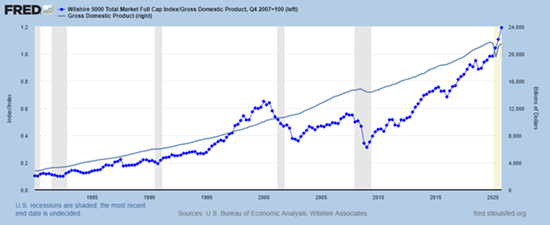

The first view is that passive investing will again pick up advocates, particularly targeted towards assets that are consistently rising (think ARK powered by Tesla et al), but given the broad participation in arguably overpriced assets it may end in tears reminiscent of the dot com period. An active management approach, at least in many portfolios, is favoured in order to put a bet down that more rational heads will prevail which may limit downside, although also limiting participation in some of the momentum driven high flyers. Active comes in all flavours and the pitch is that the best active managers find their way to the land of high fee active, aka hedge funds (although in fairness prices have come down and at least have become more aligned with investors objectives). Without the necessity of correctly identifying (a) bubble(s) in asset prices, investors at a minimum have to give some attention to measures like the one shown below, indicating that we may be at an extreme which might not continue ad infinitum.

Exhibit 1: An adaptation of Buffet’s measure of equity value shows an extreme that may not be sustainable……

If one can buy into the thesis that active management, or at least a sub-set of active management, can give investors some chance of avoiding being caught in a parade without any clothes on, it makes it interesting to parse which strategies might work best despite the state of markets. Those strategies which are most reliant on detailed corporate fundamental analysis and which lean long (including being reliant on carry) would seem to be problematic at present. This is not to say that PMs and analysts cannot perform differentiating analyses on sectors and securities, but just that they will not be rewarded in the near term as the conditions persist.

There are a sub-set of hedge fund strategies for which asset fundamental analyses are less crucial in mining alpha. One obvious place to look is in those strategies that are almost asset type agnostic and focus instead on price movements, absolute and relative. These include the broad category of CTAs/managed futures which have strategies like trend following, short-term trading, mean reversion, and pattern recognition in some combination. These have also historically been absolute sources of return in market corrections, so are perhaps dual function in this environment. Here a portfolio approach is favoured as it is difficult to dissect future performance even if provided with the algorithms. Global Macro, both discretionary and systematic, relies upon economic fundamentals and diversion amongst economies, thus is a good place to seek absolute returns, particularly with nimble managers not overly focused on directional equity. Some relative value strategies, such as volatility arbitrage, convertible arbitrage, and fixed income (non-credit), also have the advantage of not relying upon trying to gauge if asset prices are reflective of the underlying but are more concerned with assets relative to each other. Being market neutral or at least aware of mis-matches is key to staying out of pitfalls.

A thread amongst the strategies discussed is that they are either in the very liquid or liquid range of hedge funds. This allows the funds to react quickly to unfriendly changes in the markets and to deal with any liquidity squeezes. A revaluation across markets as asset prices are called into question generally is less of a concern. This exposure also provides a buffer to more risk-seeking, less liquid portions of investors’ portfolios, allowing a gentler trip through any market volatility.

Hedge funds, carefully selected by strategy and manager, have a place in both traditional and alternative portfolios despite the greatly depleted usefulness of corporate fundamentals in the current environment. Dependent on risk tolerance, portfolios can be created that actually take advantage of escalating asset prices, while having the ability to protect in a dislocation. As concerns become less about FOMO, and more about getting caught in bubble pricing, using these strategies can play some offense while providing protection.

**********

Jim Neumann is Partner and Chief Investment Officer at Sussex Partners

***

The views expressed in this article are those of the author and do not necessarily reflect the views of AlphaWeek or its publisher, The Sortino Group

© The Sortino Group Ltd

All Rights Reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or scanning or otherwise, except under the terms of the Copyright, Designs and Patents Act 1988 or under the terms of a licence issued by the Copyright Licensing Agency or other Reprographic Rights Organisation, without the written permission of the publisher. For more information about reprints from AlphaWeek, click here.